Determining Risk and Understanding the Risk Pyramid

The idea of any investment being risk-free is nothing but a farce. The degree can vary from one investment to another, but risk in investment is omnipresent. There also exists a popular concept of risk-reward, which follows the simple principle; ‘the higher the risk, the higher is the reward at the end’.

But not many investors understand how they can determine the appropriate amount of risk in their portfolios. An investor’s risk appetite can depend on a number of factors like their age, experience, financial standing, and future goals. An effective way to determine your risk tolerance is by using an investment pyramid to determine risk.

Here are some vital things to note:

Table of Contents

Understanding The Risk Reward Concept

Most investors are made to believe that higher risks get higher rewards. While this may be true to some extent, it is not entirely accurate. These statements are often made and advertised by big companies that want people to invest in their stocks. However, the returns from a risky investment can depend on many factors and profit may not necessarily always be high.

When you increase your risk capacity you also risk losing your principal amount. Some people end up letting go of their entire life’s savings over high-risk investments. The optimal level of risk in your portfolio should be based on your age, income, and future goals. It is easier for young people to cover up risk because they have plenty of time to make up for lost money. Older people who are nearing retirement do not have the luxury of time and can land up in a lot of trouble if they do not optimally distribute risk among different types of investments. It is crucial to understand the investment pyramid to analyze your risk capacity. Below are some components of a risk pyramid.

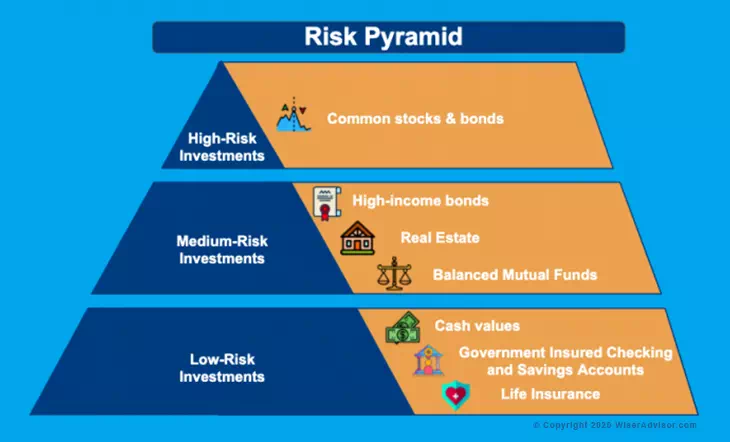

The Risk Pyramid

If you recall the shape of a pyramid, you will notice how it is wide at the bottom and keeps narrowing on its way up, to finally reach the peak. Your asset allocation and risk capacity are a lot similar to the structure of a pyramid. When you build a portfolio, you must keep this shape in mind. A balanced portfolio is a combination of low-risk assets, medium-risk assets, and high-risk investments. A risk pyramid helps you determine the percentage of each of these investments. Here’s a bifurcation of the levels of a pyramid:

The Base of the Pyramid

The bottom of the risk pyramid represents low-risk investments like cash or cash equivalents. Low-risk investments should ideally constitute the biggest chunk of your portfolio that can support the higher components in the pyramid. Try to include investments that have fixed rates of return or in simple words, investments that you can count on. Some examples are certificates of deposits (CDs), government insured checking and savings accounts, life insurance cash values, etc.

The Middle of the Pyramid

This area represents assets that come with a moderate risk capacity. Medium-risk investments are investments that offer stable returns and at the same time, the possibility of capital appreciation. Not only do these investments bring in returns, but they also appreciate in their own value. These are riskier than the investments at the bottom of the pyramid, but are still relatively safer than investments at the top. Examples of medium-risk investments include high-income bonds, balanced mutual funds, real estate, etc.

The Top of the Pyramid

The smallest area of the investment pyramid is reserved for only high-risk investments. These investments have the potential to bring in high yields but can also drop with a slight nip in the market. They also constitute the smallest part of the pyramid, so your entire portfolio doesn’t suffer in case you incur losses. Because of their serious and unpredictable nature, high-risk investments are also relatively long-term in nature. These are expected to bring high yields over a period of time and should not be seen as a means to achieve short-term financial goals. Common stocks and bonds are good examples of high-risk investments.

Need a financial advisor? Compare vetted advisors matched to your specific requirements.

Choosing the right financial advisor is daunting, especially when there are thousands of financial advisors near you. We make it easy by matching you to vetted advisors that meet your unique needs. Matched advisors are all registered with FINRA/SEC.

Click to compare vetted advisors now.Determining Risk

A risk pyramid gives an investor a good look into what their portfolio should look like. While you now know the structure of low, medium, and high-risk investments in your portfolio, you must also consider the different types of investment methods in each of these categories. For example, you can choose from government bonds, money market accounts, or a savings account for the base of your investment pyramid. So how do you pick the best method for your financial needs?

Here’s what you should consider:

Time

Needless to say, time plays a very important role in deciding the right investment for your portfolio. You should be aware of the time for which you are required to keep your money in a particular investment. For example, high-risk investments require a longer time-frame to mature into good returns. The volatility of the market would typically result in loss over a shorter duration. So, if you are looking to use up the money from an investment in the next year, you should look for low-risk or medium-risk investments. Always remember that a high-risk investment needs more time to be able to recover from probable losses. You must keep all your future goals in mind before drafting out a portfolio.

Comfort

Your tolerance and comfort for risk are both important factors when deciding on an investment. It is never advisable to just follow trends or tactlessly invest your money in the next big thing. Every person’s comfort in relation to risk is different. Ascertain how much you can afford to put at stake before you begin to lose sleep at night. If you have a bigger risk capacity, settling for conservative investments will never sit well with you, or vice versa. Remember that investing money should bring you satisfaction, a sense of relief, and confidence that your money can bring in high returns. There is no point in fretting over returns at the cost of your mental peace.

Financial standing

While taking well calculated high-risks can possibly result in higher yields, remember that there is never any guarantee when it comes to investing. The market is an unpredictable space, so it is important to be realistic of your financial standing. A loss of $5,000 can have different implications for different people. Understand how much money you can afford to lose and be prepared for the ‘worst-case scenario’. Always be pragmatic about your net income before determining your risk capacity.

To sum it up

Risk is inevitable. But, with a correct strategy in place and proper understanding of future goals, investors can tackle it efficiently. To allocate the right investments in your investment pyramid, you need to carefully assess all your sources of income and decide on your risk capacity. Divide your goals into short-term, mid-term, and long-term and then distribute your money around the pyramid. You should be aware of the time and money that you need to put in an investment before it matures to bring back good returns, or else the entire process can be frustrating and tiresome.

Does your investment pyramid match your risk appetite? Contact financial advisors to devise the best-suited investment allocation for you.

A team of dedicated writers, editors and finance specialists sharing their insights, expertise and industry knowledge to help individuals live their best financial life and reach their personal financial goals. We believe that there is no place for fear in anyone's financial future and that each individual should have easy access to credible financial advice.

Related Article

8 min read

18 Sep 2025

5 Step Guide on Building Wealth

By the time you reach the midpoint of your career, the financial landscape changes. Instead of starting to save, the urgency is more about making your money work harder, faster, and more predictably. Retirement is now a visible point on the horizon, and thus, every decision now carries more weight as the margin for error […]

10 min read

16 Sep 2025

Wealth Creation vs Wealth Preservation: What Matters Most as You Near Retirement

In your 30s and 40s, the financial conversation often revolves around maximizing returns, growing your portfolio, and building momentum. But by the time you reach your 50s and early 60s, a different question takes center stage: How do I protect what I’ve built? That’s where the distinction between wealth creation vs wealth preservation becomes strategic. […]

10 min read

05 Sep 2025

Everything You Need to Know About Balanced Funds

Convenience, thy name is mutual funds! Mutual funds have really simplified how the world invests. Gone are the days when building a portfolio meant spending hours handpicking individual stocks and bonds. You had to keep one eye on market news and another on price movements, while still finding time to decide when to buy or […]

9 min read

04 Jul 2025

What are the Tax Brackets and Federal Income Tax Rates for the 2025-2026 Tax Year?

Did you know that the Internal Revenue Service (IRS) adjusts 2025 tax brackets to account for inflation? Yes! The numbers you saw on your 2024 return probably will not be the same in 2025. These changes can affect how much tax you owe and whether you are eligible for certain tax credits or deductions. But […]

More From Author

14 min read

23 Jan 2024

How to Determine If Your Financial Advisor Is Doing a Good Job Each Year

The decision to hire a financial advisor is a prudent move. Seeking professional advice can provide valuable insights and a roadmap to achieve your financial goals with strategic planning. But the world of financial advice is crowded. While some advisors bring qualifications, expertise, and a commitment to your financial well-being, others may fall short of […]

4 min read

30 Oct 2023

How to prepare for a meeting with your Financial Advisor

What do you do before you visit a doctor? Understand your condition, prepare for all the questions that the doctor would ask, ensure all your test reports and medical history documents are in order and so on. Preparation is a must even before you visit a financial advisor. Table of Contents7 Things to do to […]

3 min read

26 Jul 2019

Best Retirement Calculators to plan Retirement

It is said that a goal without a plan is just a wish. This holds true even for retirement planning. You dream of a peaceful retired life. To achieve that you must plan for your golden years well in time. Various retirement tools make your task easier. For example, a retirement calculator helps you calculate […]

4 min read

23 Mar 2020

How to get rid of Money Anxiety?

Is money anxiety even a thing? Yes, it is! Money anxiety is something we all have dealt with or are likely to deal with at some point in our life. Sometimes, you may not even know that you are money anxious unless you take note of it. But the good part here is that money […]

Find & Compare Top Financial

Advisors in your area

Get Started

Popular Posts

Categories

- Business Finance (2)

- Education Planning (31)

- Estate Planning (31)

- Financial Advisor (1)

- Financial Advisor Guide (55)

- Financial Planning (138)

- Investment Management (99)

- Personal Finance (15)

- Portfolio Management (1)

- Retirement (30)

- Retirement Healthcare (1)

- Retirement Planning (109)

- Retirement Plans (1)

- Uncategorized (4)

Subscribe to our

newsletter & get helpful

financial tips.

The blog articles on this website are provided for general educational and informational purposes only, and no content included is intended to be used as financial or legal advice. A professional financial advisor should be consulted prior to making any investment decisions. Each person’s financial situation is unique, and your advisor would be able to provide you with the financial information and advice related to your financial situation.